Tax Deduction for Corporation Donating Inventory

Tax Deduction for Corporation Donating Inventory

Seek professional help today if you are around DFW and need guidance on tax deduction for corporation donating to ensure the company’s enduring success and lower the cost!

TAX KNOWLEDGE

1/16/20252 min read

1. General Rule

Basic Deduction Rules

Corporations can deduct charitable contributions of inventory, but the deduction is generally limited to the smaller of the fair market value (FMV) or the basis of the donated inventory

The basis is typically the cost incurred for the inventory in an earlier year that would have been included in the opening inventory for the year of the contribution

Limitations and Considerations

The general deduction limit for corporate charitable contributions is 10% of pretax income

Excess donations can be carried forward for five years

2. Enhanced Deduction Under 170(e)(3)

Section 170(e)(3) provides an exception to this general rule. This deduction is only available for C corporations and is only helpful for those that are on the accrual method.

A C corporation can claim an enhanced deduction for inventory donations if:

-

The donation is to a public charity (not a private foundation);

-

The property will be used solely for care of the ill, needy, or infants;

-

The charity cannot charge for the donated items;

-

The donor receives a written statement from the charity confirming these requirements; and

-

If the property is regulated (like food or drugs), it meets applicable regulations

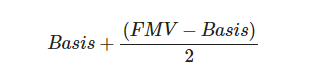

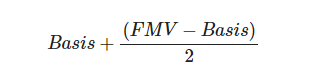

The enhanced deduction amount is tax basis plus half of the appreciation. So the fair market value minus tax basis. These combined amounts cannot exceed twice the amount of the tax basis

Definition of Ill, Needy, and Infant

To qualify for the enhanced deduction the property must be used solely for the care of the “ill, needy, or infants.” The regulations provide detailed definitions for each of these categories:

The regulations define an “ill person” as one requiring medical care. This includes individuals:

-

Suffering from physical injury

-

With significant impairment of a bodily organ

-

With an existing handicap (whether from birth or later injury)

-

Suffering from malnutrition

-

With a disease, sickness, or infection significantly impairing physical health

-

Partially or totally incapable of self-care (including due to old age)

-

With mental illness if hospitalized/institutionalized or if the illness constitutes a significant health impairment

A “needy person” is defined as one who lacks life’s necessities involving physical, mental, or emotional well-being due to poverty or temporary distress. Examples include:

-

Those financially impoverished due to low income

-

Individuals temporarily lacking food or shelter

-

Victims of natural disasters (like fires or floods)

-

Victims of civil disasters

-

Those temporarily not self-sufficient due to sudden crisis

-

Refugees or immigrants experiencing language, cultural, or financial difficulties

-

Former prisoners or mental institution patients who are not self-sufficient

The regulations define an “infant” as a minor child, as determined under the laws of the jurisdiction where the child resides. The “care of an infant” means performing parental functions and providing for the child’s physical, mental, and emotional needs.